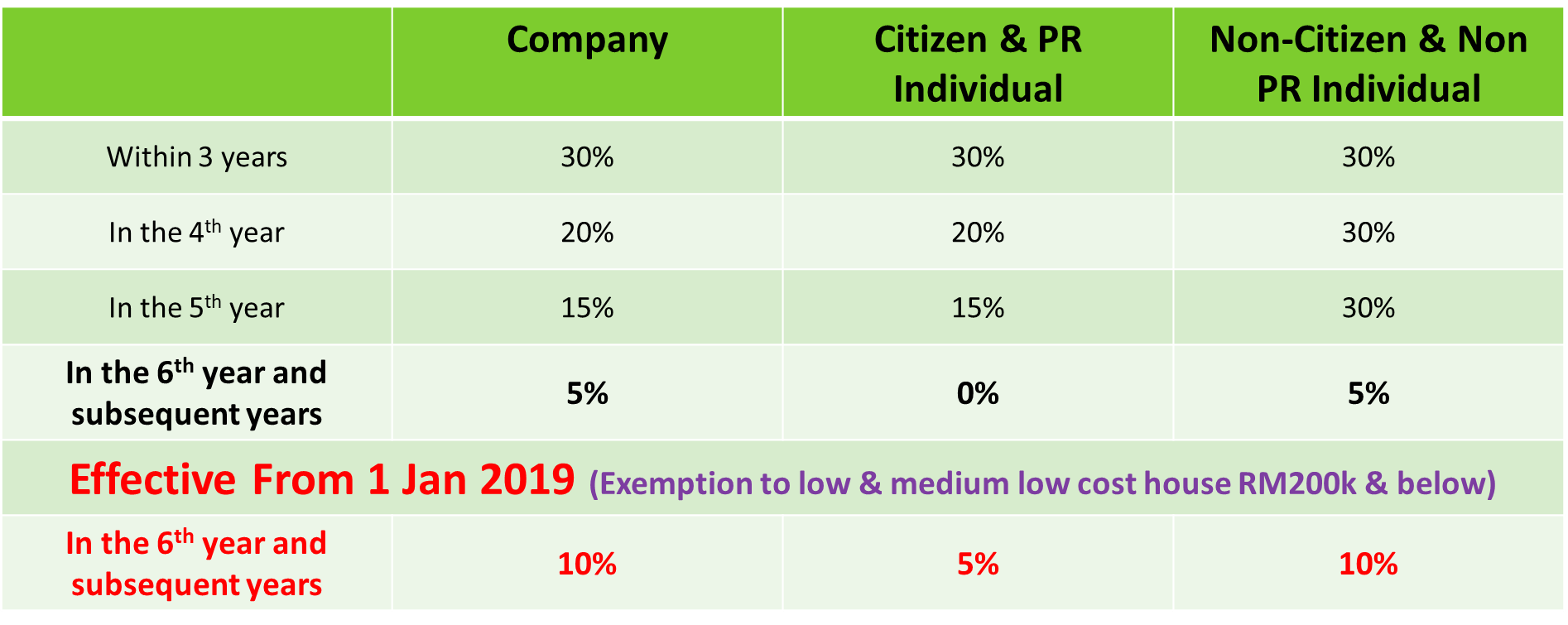

What Is Capital Allowance In Taxation Malaysia

Chapter 7 Capital Allowances Students

Malaysia Taxation Junior Diary Capital Allowance Schedulers

Solved Malaysia Taxation Question Chegg Com

Preparing The Capital Allowance Computation Acca Taxation Tx Uk Youtube

Capital Allowance Rate For Computer Software Malaysia

Chapter 7 Capital Allowances Students

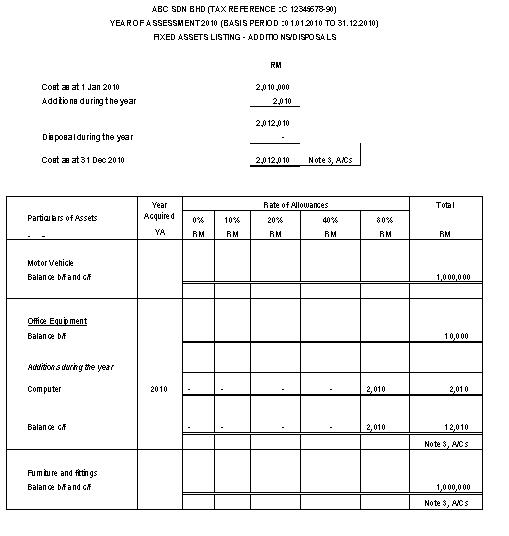

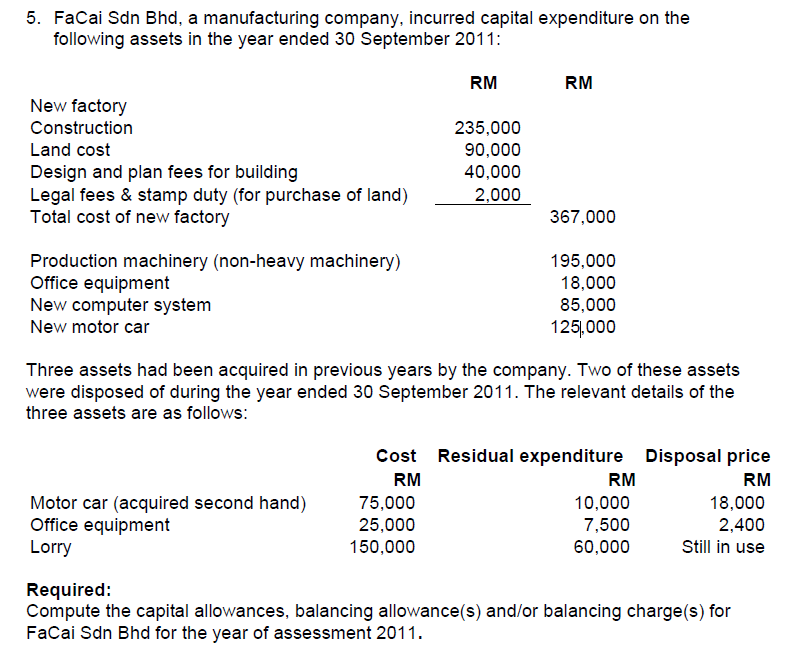

Some examples of assets that are normally used in business are motor vehicles machines office equipments and furniture.

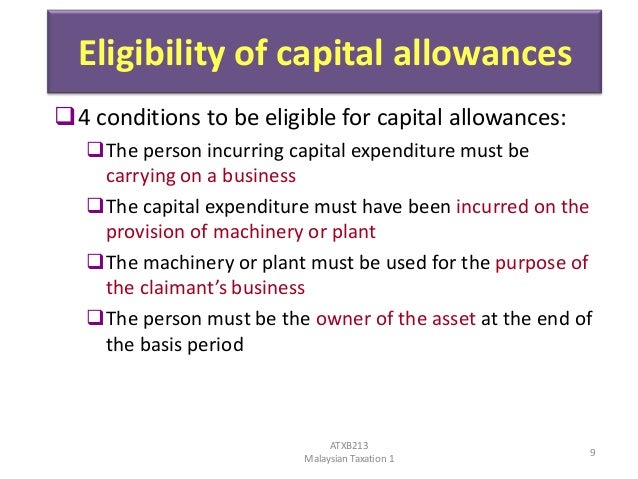

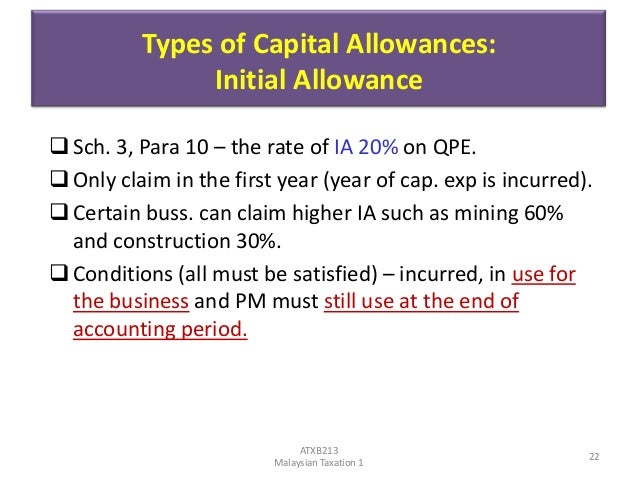

What is capital allowance in taxation malaysia. Conditions for claiming capital allowance are. The balancing charge is restricted to the amount of allowances previously claimed. Initial allowance is granted in the year the expenditure is incurred and the asset is in use for the purpose of the business. Relevant provisions of the law 3 1 this pr takes into account laws which are in force as at the date this pr is published.

Capital allowance tax depreciation on industrial buildings plant and machinery is available at prescribed rates for all types of businesses. And b computation of capital allowances for expenditure on plant and machinery. In the current tax environment in malaysia the amount of tax declared by a taxpayer would constitute its own tax assessment. Income tax accelerated capital allowance security control equipment.

27 june 2014 page 2 of 28 3. 5 2014 date of publication. 3 2 the provisions of the income tax act 1967 ita related to this pr are. It is only calculated when a company is computing its tax liabilities.

Capital allowance is only applicable to business activity and not for individual. Capital allowance is a claim against assessable profits by companies when computing their tax liabilities. However schedule 3 of the income tax act 1967 has laid down several allowable deductions in the form of allowances for the capital expenditures that have been incurred. Inland revenue board of malaysia date of issue accelerate capital allowance public ruling no.

Capital allowance is only given to business activity. Balancing adjustments allowance charge will arise on the disposal of assets on which capital allowances have been claimed. Capital allowance is given as deduction from business income in place of depreciation expenses incurred in purchase of business assets. However there are different methods of calculating depreciation which.

15 april 2013 page 2 of 34 2 14. Relevant provisions of the law 2 1 this pr takes into account laws which are in force as at the date this pr is published. A tax treatment in relation to qualifying expenditure on plant and machinery for the purpose of claiming capital allowances. Generally the balancing adjustment is the difference between the tax written down value and the disposal proceeds.

The purpose of capital allowance is to give a relief for wear and tear of fixed assets for business. Usually when companies prepare income statement they always charge depreciation as an expense before arriving at their profit before tax.

Malaysia Taxation Junior Diary Capital Allowance Schedulers

Icapitaleducation Biz Malaysia S First Integrated Investment Education Provider

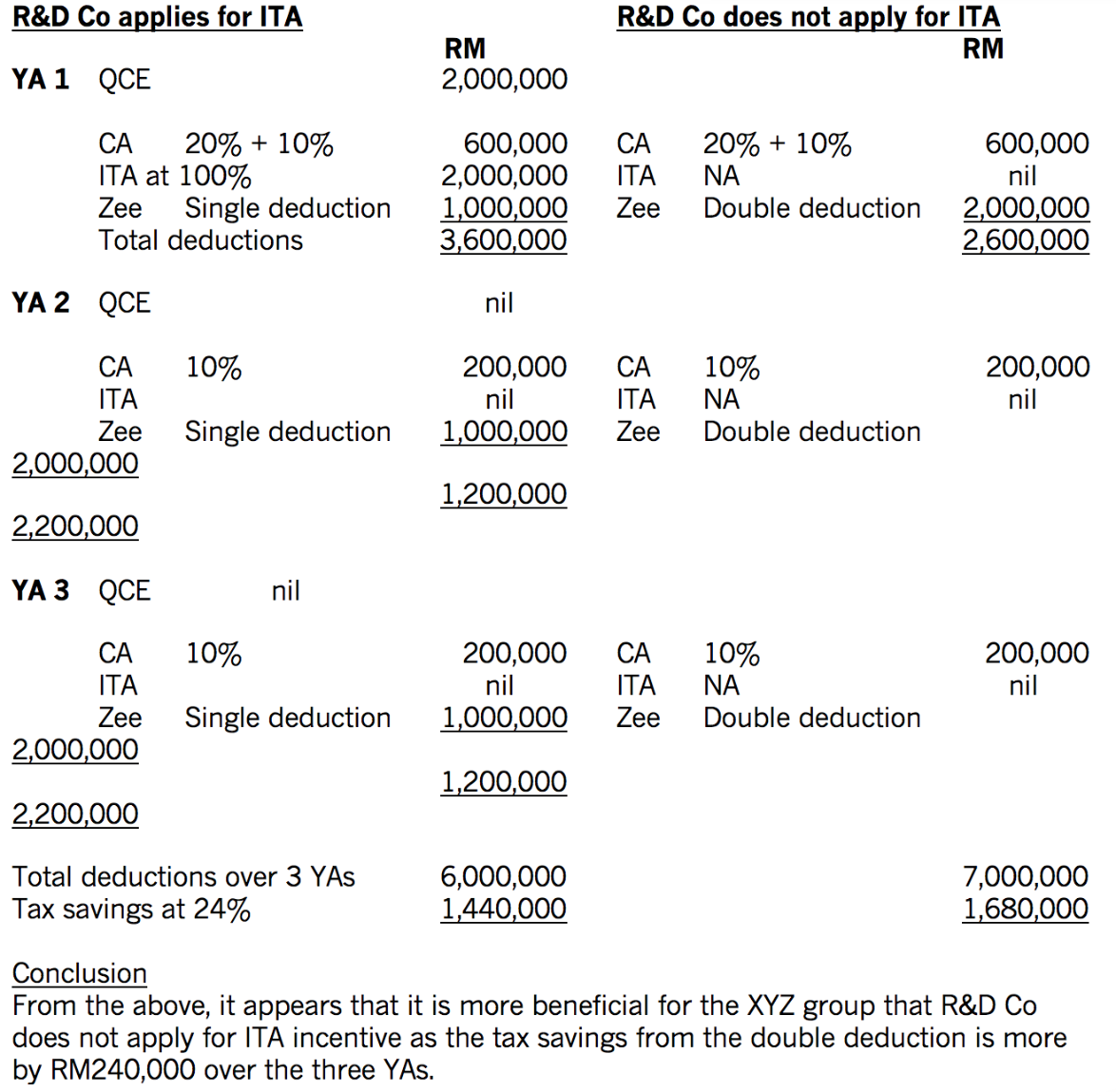

Tax Incentives For Research And Development In Malaysia Acca Global

Chapter 7 Capital Allowances Students

Tax Planning For Business Assets The Star

Capital Allowances Recent Changes To Rates Thresholds Etc Tax Uk

Smeinfo Understanding Tax

P6 F6 Capital Allowance Non Commercial Motor Vehicle With Hp Youtube

Estimated Chargeable Income A Step By Step Guide To Calculating Eci

Https Www Accaglobal Com Content Dam Acca Global Pdf Students 2012s Sa Aug12 F6 Vehicles Pdf

Chapter 7 Capital Allowances Students

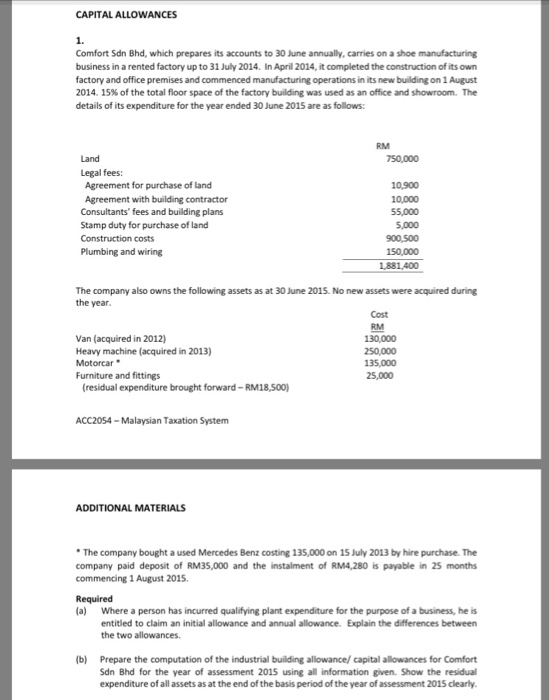

Solved Capital Allowances 1 Comfort Sdn Bhd Which Prepa Chegg Com

Malaysia Taxation Junior Diary Capital Allowance Schedulers